As we settle into 2026, many of our senior policyholders are receiving renewal notices that look significantly different from last year’s. We understand the anxiety this causes. For our clients aged 60 and above, the arrival of a premium notice with a hike of approximately 30% is a heavy financial blow, especially for those on fixed pension incomes.

As your insurance partners, Medicard.my believes in transparency. It is crucial to move beyond the sticker shock and understand why this is happening, what the industry landscape looks like, and most importantly, what options remain available to you to ensure you are not left unprotected.

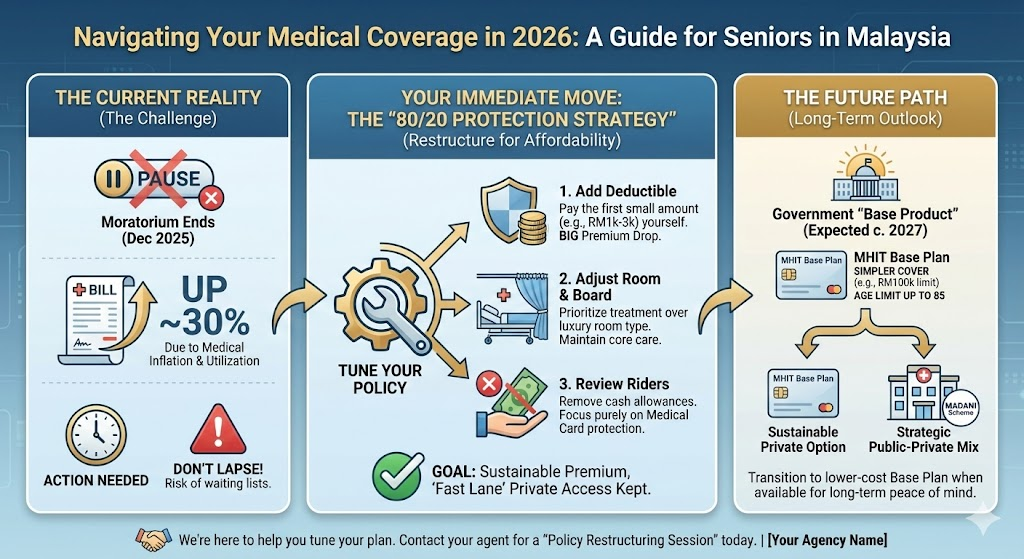

The Context: The End of the Moratorium

In December 2024, Bank Negara Malaysia (BNM) announced a compassionate measure: a temporary freeze on premium adjustments for policyholders aged 60 and above. This was a move to buffer seniors against the rising tide of costs. That one-year pause has now concluded.

While an official industry-wide announcement is expected later this month, the reality is already here. Insurers are issuing notices based on current actuarial calculations. The “catch-up” effect of pausing prices while medical costs continued to rise has resulted in the steep adjustments—averaging around 30%—that many are seeing now.

The Core Driver: Medical Inflation vs. General Inflation

The most common question we get is: “Inflation is only 2-3%, why is my premium going up by 30%?”

It is vital to distinguish Medical Inflation from general inflation (CPI). In Malaysia, medical inflation frequently hits double digits, often outpacing the general economy by 3 to 4 times.

- New Technologies: Advanced treatments (like robotic surgeries or targeted cancer therapies) save lives but cost significantly more.

- Rising Hospital Costs: The cost of running private hospitals—from nursing wages to imported medical supplies—has skyrocketed.

- Utilization: As a population, we are utilizing medical cards more frequently for chronic illnesses than ever before.

Insurers are no longer able to customize plans freely; we are bound by strict actuarial guidelines set by Bank Negara to ensure the insurance fund remains solvent enough to pay claims in the long run.

The Risks of Lapsing

We are hearing heartbreaking stories from the ground—of retirees considering returning to the workforce or borrowing money just to keep their policies active. Some are choosing to let their policies lapse entirely.

We strongly urge you to pause before canceling your policy.

The public healthcare system in Malaysia is excellent but overwhelmed. Recent reports highlight that waiting lists for critical procedures, such as heart bypass surgeries, can extend up to two years at government facilities. For a senior citizen with a deteriorating condition, time is a luxury you may not have. Your medical card is not just a plastic card; it is your “fast lane” to immediate treatment.

Looking Ahead: Potential Relief on the Horizon

The situation is being monitored at the highest levels. The Joint Ministerial Committee on Private Healthcare Costs (JMCPHC) is currently reviewing the landscape. While premiums may remain high through 2027, there are discussions about regulating premiums for the elderly specifically.

Furthermore, the government is reportedly working on a new base product. Early sources suggest this could offer coverage of up to RM100,000 and extend eligibility up to age 85. This could serve as a vital safety net for those who can no longer afford comprehensive private riders but still need basic protection.

What Can You Do Now?

If you have received a notice and are struggling to pay the new premium:

- Do Not Ignore the Notice: Ignoring it could lead to an automatic lapse. Once a policy lapses, getting a new one at a senior age is often impossible or comes with exclusions for pre-existing conditions.

- Speak to Your Agent Immediately: Ask for a Policy Review.

- Can we increase the deductible? (Paying the first RM500 or RM1,000 yourself can lower the premium significantly).

- Can we remove non-essential riders? (Focus on the room and board and surgical fees; drop the cash allowances if budget is tight).

- Ask About “Downgrading” Options: It is better to have a lower annual limit (e.g., RM100,000 instead of RM1 million) than to have zero coverage.

Our Commitment

We know this is a difficult transition period. Our agency is committed to helping you find a sustainable balance between affordability and protection. Please reach out to our team—we are here to calculate the numbers with you and explore every avenue to keep you covered.

Our Mission: The 80/20 Protection Strategy

At Medicard.my, our specific mission is to ensure our clients aged 60 and above can maintain sufficient coverage without breaking the bank. We understand that a standard policy may no longer fit a retiree’s budget. Therefore, we are committed to customizing a plan that aligns with your specific risk profile to achieve an “80/20 effect.”

Our goal is to structure your policy so that the premium remains affordable (the 20% input) while you still retain the critical protection needed against severe illnesses (the 80% output). By analyzing your health history and risk factors, we can adjust variables—such as room and board rates or deductible options—to strip away unnecessary costs while keeping the core safety net intact. We want to ensure the premium is not burdensome, yet you have the peace of mind that if a major health crisis strikes, your medical card will still be there to shield you.

The Senior Policy Restructuring Checklist

Goal: Achieve the “80/20 Effect”—Maximum Protection for an Affordable Premium.

Before you decide to cancel or lapse your policy due to the recent price hikes, go through this checklist with your insurance agent. We can often “tune” these settings to lower your monthly commitment while keeping your medical safety net intact.

1. 🔲 Review Your Deductible Options

- The Question: “Can I add a deductible of RM500, RM1,000, or RM3,000?”

- Why: Agreeing to pay the first small portion of a hospital bill can reduce your annual premium significantly (sometimes by 15-25%).

- The Strategy: Use your personal savings for minor ailments, but keep the insurance for the big, expensive surgeries.

2. 🔲 Adjust Room & Board (R&B) Entitlement

- The Question: “Am I paying extra for a Single Room (e.g., RM250+) entitlement? Can I lower this?”

- Why: Room rates inflate the base premium.

- The Strategy: Downgrading to a shared room (2-bedded) or a lower R&B rate can save costs. The medical treatment remains exactly the same; only the accommodation changes.

3. 🔲 Re-evaluate Annual Limits

- The Question: “Do I really need RM1 million or Unlimited coverage right now?”

- Why: Super-high limits cost more.

- The Strategy: An annual limit of RM150,000 – RM200,000 is often sufficient for most severe local treatments (like bypass or cancer therapy) in private hospitals. We can check if a “base plan” is available.

4. 🔲 Audit Your Riders (The “Nice-to-Haves”)

- The Question: “Am I paying for ‘Hospital Income’ or ‘Cash Allowance’ riders?”

- Why: These riders pay you cash when you are hospitalized, but they are expensive additions.

- The Strategy: Remove these cash benefits. Focus your budget purely on the Medical Card (paying the hospital bill), which is the absolute necessity.

5. 🔲 Check Payment Frequency

- The Question: “Am I paying Annually? Can I switch to Monthly or Quarterly to help cash flow?”

- Why: While annual is sometimes cheaper, breaking it down into smaller monthly chunks can make the RM5,000+ bill manageable for a retiree’s monthly pension.

6. 🔲 The “Smart Saver” Review (Co-Takaful/Co-Insurance)

- The Question: “Is there a Smart Saver option where I pay 10% of the bill (capped at a maximum, e.g., RM3,000)?”

- Why: Similar to deductibles, sharing a small risk with the insurer drastically lowers the premium price.

7. 🔲 Critical Dates Check

- The Question: “Exactly when does my policy lapse?”

- Why: Know your grace period (usually 30 days). Ensure you make a decision before this date to avoid a health check-up requirement for reinstatement.

For people aged 60 and above facing this specific crisis in Malaysia (2026), the “best case” scenario is not a single magic bullet, but rather a combination of successful policy restructuring today and a government-backed transition in the near future.

Here is the realistic “Best Case Scenario” broken down into three tiers:

1. The “Immediate” Best Case: Successful ‘Downsizing’ (The 80/20 Win)

The best immediate outcome is that you keep your private status but shed the “luxury” weight of your policy.

- The Scenario: You successfully renegotiate your policy with your agent. instead of paying the new RM6,400+ premium, you switch to a High Deductible Plan (e.g., agreeing to pay the first RM3,000–RM5,000 of any bill).

- The Result: Your premium drops by 30-40%, bringing it back to a manageable level (e.g., RM3,500 – RM4,000).

- Why this is a win: You retain your “Fast Lane” card. If you have a heart attack or stroke, you still go to a private hospital immediately. You only pay the first portion (using savings), and the insurance covers the massive remainder. This avoids the 2-year government waiting list mentioned in the news.

2. The “Future” Best Case: The New ‘Base Product’ (MHIT)

This is the “Golden Hope” currently being worked on by the government (Ministry of Finance & Bank Negara), expected to fully launch around 2027.

- The Scenario: You hold on to your current expensive policy for just one more year (2026). By 2027, the government launches the new Medical and Health Insurance/Takaful (MHIT) Base Product.

- The Product: It is a standalone “pure protection” plan (no investment linkage).

- Coverage: Likely capped at RM100,000 annually (sufficient for most single critical surgeries).

- Age Limit: Entry/renewal up to Age 85.

- Cost: Significantly cheaper because it strips away all “bells and whistles” and marketing costs.

- The Result: You transition from your expensive private plan to this government-regulated base plan. You are protected for the “big stuff” at a price a pensioner can actually afford.

3. The “Hybrid” Best Case: The Public-Private Mix

If private premiums are truly impossible to pay, the best case is a strategic use of both systems rather than a total loss of care.

- The Scenario: You let the expensive private medical card lapse but sign up for the Madani Medical Scheme (if eligible/B40) and rely on the public system for major surgeries.

- The Strategy:

- Minor Ills (Fever/Flu): Use the Madani Medical Scheme to visit private GPs for free (government-paid), avoiding the congestion of public clinics.

- Major/Non-Emergency (Cataracts/Knee Replacement): You join the government hospital queue (Wait time: 6–12 months).

- Critical Emergency (Heart Attack/Accident): You go to the Government Hospital Emergency Department. Emergency cases are treated immediately in public hospitals, bypassing the queue.

- The Win: You pay RM0 in premiums. You sacrifice “comfort” and “speed for non-critical issues,” but you receive high-quality medical care for free.

Summary of the “Best Case” Path

The ideal path for a senior citizen right now is:

- Restructure NOW: Downgrade your current plan (increase deductible) to survive 2026.

- Wait for 2027: Keep your eyes peeled for the government’s Base MHIT Product.

- Switch Later: Move to the Base Product when it launches for long-term sustainability up to age 85.