As Malaysia’s leading medical card expert, Medicard.my has always received a lot of feedback on how expensive or unaffordable medical insurance coverage is for the normal everyday Malaysian. As someone who has endured great financial difficulties due to care for my parents, I understand how important it is to maintain a good medical card for as long as possible. My mother, who passed away in February 2024, had zero medical coverage at age 66 – the time of her passing. She had suffered from an infection and had gone into coma all of a sudden. We thought it was just a skin infection – it turned out to be much worse than our expectation. She was admitted into ICU of Sunway Medical Center – one of the best private health care institutions in Malaysia. She had never recovered from her coma – and passed away after 4 days of fighting for her life.

The total medical cost for her hospitalisation at Sunway Medical Center was RM 95,000. We had to pay for that expense out of pocket. So I definitely have first hand experience of how debilitating it is to not have medical coverage and how difficult it is to raise enough cash to pay for the treatment. We had to use multiple credit cards.

Anyway… enough of my sob story. The reason why I am writing this is because a lot of complaints from our readers saying how impossibly unaffordable a medical coverage is in Malaysia nowadays.

The first way to looking at things here: Balancing medical card coverage with your income is an exercise in risk management: you want to pay as little as possible while ensuring you don’t go bankrupt from a hospital bill. The key goal is to prevent total financial collapse from a medical emergency. It is not how much coverage you need over a lifetime, what kind of private hospital suite you want when you get admitted. Financial protection is key, not comfort.

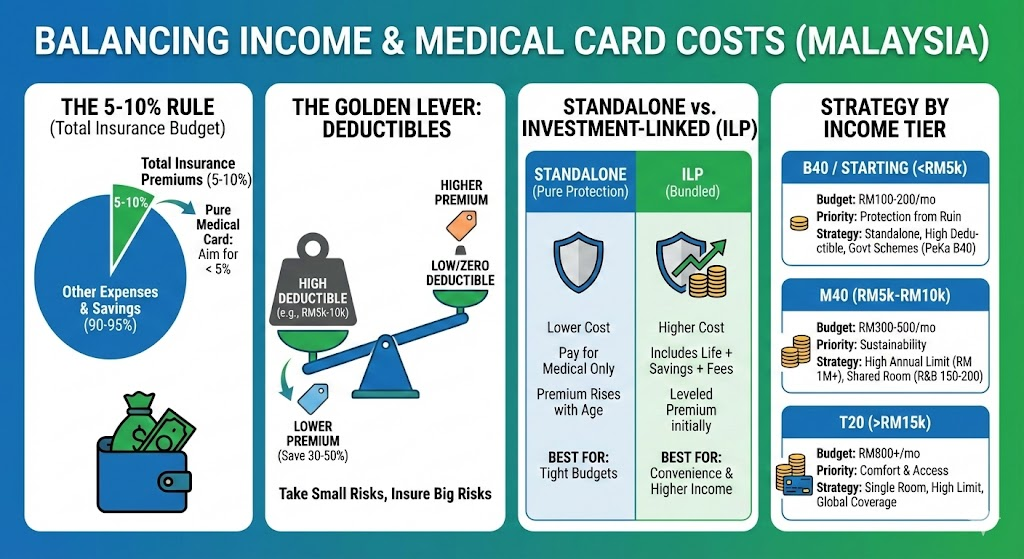

In Malaysia, a common financial planning rule of thumb is that your total insurance premiums (medical + life + critical illness) should strictly be between 5% and 10% of your monthly income. Ideally, purely medical coverage should not exceed 5%. Anything around this is a good figure. So ideally speaking 10 percent of your income (more or less) should be spent on a decent medical/life insurance coverage.

Use Deductibles to Save on Monthly Costs:

The single most effective way to lower your monthly premium without lowering your protection limit is to choose a plan with a Deductible.

- How it works: You agree to pay the first portion of the bill (e.g., RM500, RM5,000, or RM20,000) before the insurance kicks in.

- The Strategy: If you have RM10,000 in emergency savings, buy a medical card with a RM5,000 or RM10,000 deductible.

- The Result: Your monthly premium can drop significantly (sometimes by 30-50%) because you are taking on the “small risks” (fevers, minor injuries) yourself, while the insurer only covers “catastrophic risks” (cancer, major surgeries).

Standalone vs. Investment-Linked (ILP)

Understand the structure you are buying, as this dictates cash flow.

| Feature | Standalone Medical Card | Investment-Linked Policy (ILP) |

| Cost | Cheaper (Pure insurance). | More Expensive (Bundled with life insurance & savings). |

| Structure | You pay only for medical coverage. | You pay for medical + life + agent commissions + investment units. |

| Premium Trend | Increases noticeably as you get older (every 5 years). | Premiums are generally “leveled” (flat) early on, but risk charges increase internally. |

| Best For | Strict budgeters who want maximum medical coverage for the lowest monthly price. | People who want convenience (all-in-one) and can afford higher upfront monthly commitments. |

Verdict: If your income is tight, buy a Standalone Medical Card. Do not mix insurance with investment; keep them separate to keep fixed costs low.

Adjust “Room & Board” (R&B)

Medical cards are often priced based on the daily room rate they cover (e.g., R&B 150, R&B 200, R&B 500).

The Balance: Accept a “Four-Bedded” or “Two-Bedded” room plan (R&B 150-200). The medical treatment (doctors, surgery, medicine) is usually fully covered regardless of the room type. You are there to get treated, not for a hotel stay.

The Trap: Wanting a “Single Room” often forces you into a premium tier that is 20-30% more expensive.

Review Your Employer’s Medical Coverage Benefit

Most employees in Malaysia have Group Hospitalization and Surgical (GHS) insurance.

- Scenario: Your company covers you up to RM50,000 per year.

- The Strategy: You don’t need a “zero deductible” personal card. Buy a personal card with a high deductible (e.g., RM20,000).

- In Practice: If you are hospitalized, use your Company Card to pay the first RM20,000. Use your Personal Card to cover anything above that. This allows you to hold a cheap personal policy that only activates for major disasters.

As We Become Older, What Can We Do to Deal with Rising Insurance Premiums that Often Exceed Our 10 percent Income Rule?

As you get older, insurance becomes much more expensive because older people are more likely to get sick, creating a financial trap just as your income drops in retirement. This problem is made worse because hospital prices rise very fast every year, often draining the “savings” inside your insurance policy and forcing you to pay huge extra fees later on. To keep your coverage affordable without cancelling it, you should adjust your plan early: switch to a “deductible” plan (where you pay the first small amount, like RM5,000, to get a huge discount on your monthly fee), choose a cheaper shared room, or use a low-cost private card for quick emergencies while relying on government hospitals for expensive, long-term treatments.

Buying insurance and never looking at it again is risky because hospital prices rise every year, making your old coverage insufficient without you realizing it. A quick review every two years acts like a “health check” for your policy, helping you spot gaps early—such as a room limit that is now too low or a cash value that is running out. It is much safer to make small, affordable adjustments today than to face the terrible surprise of finding out your medical card won’t pay the bill right when you are standing at the hospital admission desk.